The following is an extract from the in-house analysis to determine if CuBit™ is a security or a commodity / currency. For the full document click here.

CuBit™ and the Howey Test

In-house Analysis

August 2024

Foreword

The Howey analysis of CuBit™ was originally performed in November of 2022. Since then, the regulatory picture has become much clearer.

The classification of Bitcoin (BTC) and Ethereum (ETH) as commodities unequivocally took them out of the realm of securities. On the securities side, the creation of exchange traded funds (ETF) for both BTC and ETH opened a well-regulated avenue for industrial investors to put their money into cryptocurrencies on an equal footing with other commodities trading.

UREWPS believes that these developments, and the structure of CuBit™ moot the point-by-point discussion of how this receipt cryptocurrency fails the Howey test. Regardless, it is still helpful to many readers to understand exactly why CuBit™ is appropriately exempt from securities laws.

Introduction

Consideration of whether CuBit™ qualifies as a security requires understanding the principal test used in US Law to figure out what constitutes a security. The US Supreme Court’s Howey case and later case law are our best guides. We expect the most reliable interpretation of these frameworks is found on the official website of the Securities and Exchange Commission (SEC): www.sec.gov.

The analysis below breaks down the Framework for “Investment Contract” Analysis of Digital Assets, as found on the SEC site, point by point as it relates to CuBit™. For a full explanation of CuBit™, please read the CuBit™ Whitepaper.

Application of Howey to Digital Assets

There are three key points in the so-called Howey Test:

- Investment of Money

- Common Enterprise

- Reasonable Expectation of Profits Derived from Efforts of Others

The first two points are so universally applicable to any enterprise that they are uncontestable for CuBit™. This leads us to dissect and respond only to the elements of the third prong of Howey. Additionally, the cited article notes some other relevant considerations which we also address.

The third test in Howey has two subsections:

- Reliance on the Efforts of Others

- Reasonable Expectation of Profits

Regarding reliance on the efforts of others, UREWPS concedes that there is no worthwhile endeavor which can succeed without the cooperation of others. Even the farmer who plants, waters, harvests, and sells his own crops is dependent upon the manufacturer of irrigation systems, planting machinery, harvesters, pesticides, cargo trucks, etc. Therefore, it is unrealistic to believe that any endeavor can be carried to fruition without reliance on the efforts of others.

CuBit™ Context

To consider the following points about a reasonable expectation of profits it is first necessary to understand the purpose and intent of CuBit™, and its structure. We will begin with the structure.

Structure of CuBit™

CuBit™ is a blockchain smart contract using the ERC-20 standard contract protocol on the Ethereum Mainnet blockchain. Without trying to explain all these terms further we will say that what is important to understand from this is that CuBit™ is not creating a network, or a new blockchain to support its functionality. In short, the value of CuBit™, today or tomorrow, is not dependent in any way on further development of any network.

Purpose and Intent of CuBit™

CuBit™ is intended to function as a vehicle for depositors to keep their wealth stored relatively safely from the effects of inflation and market volatility. Regardless of all precautions, CuBit™ cannot guarantee inflation or volatility will not degrade the value of deposits. No economic vehicle is immune to catastrophic economic events.

Reasonable Expectation of Profits

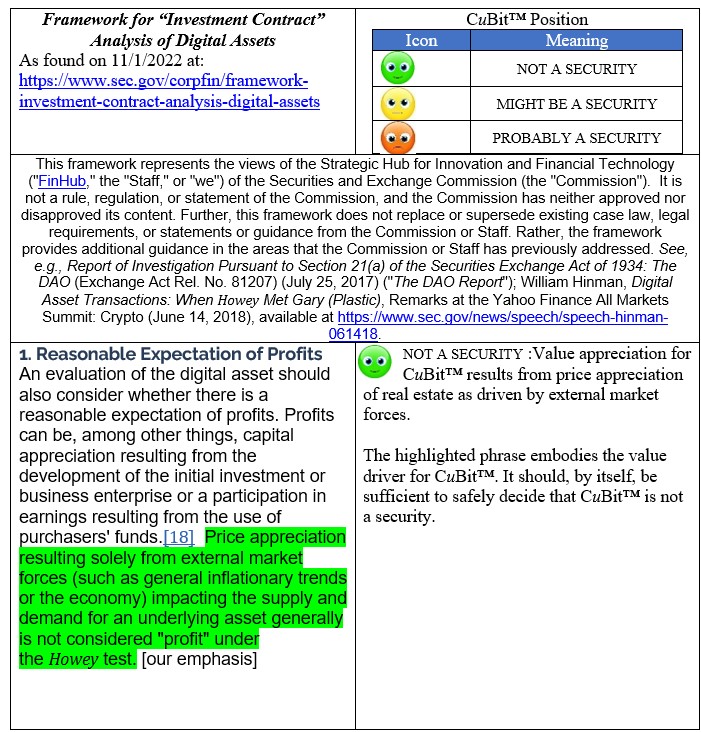

While it might be convenient for readers to push the following table (See Table 1) into an appendix, we have opted instead to include this here as it embodies the primary points of this paper. The left column has intact, direct excerpts from the cited article. The right column has the CuBit™ position compared to the point cited in the left column.

Key Exemption

In the third row of the table below is a key exemption which applies to CuBit™.

“Price appreciation driven solely by external market forces (such as inflationary trends or the economy) impacting the supply and demand for an underlying asset generally is not considered ‘profit’ under the Howey test.”

All value changes expected for CuBit™ are designed to derive from real estate appreciation.

These changes are expected to be sufficient to offset increases in inflation. CuBit™ is designed to prevent extreme variations in its value independent of extreme changes in inflation. It achieves this through two mechanisms:

- a geographically diversified real estate portfolio across the USA

- diversified real estate types (e.g., single family, multi-family, commercial, etc.)

The reliance of CuBit™ value changes on external market forces is sufficient, by itself, to decide that CuBit™ is not a security. Regardless, we address all the remaining points individually in the table below. In most cases, failing a test point below means CuBit™ is not a security. However, some test points need to be ‘passed’ to indicate CuBit™ is not a security.

Since we do not believe CuBit™ is a security we are pleased when a point demonstrates CuBit™ is not a security. To clarify our views, we have added icons to the table which show when an answer pleases us.

To see the whole table you will need to download the full analysis by clicking the button below or by clicking here

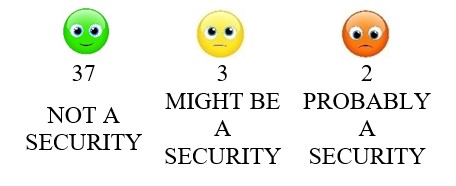

Keeping Score

With thirty-seven of forty-two points indicating that CuBit™ is probably not a security, CuBit™ fails Howey. Failing the Howey test means the issue is not a security. The answers in the “consumption characteristics”, included in the additional considerations, show that CuBit™ has consumption characteristics of a currency rather than those of a security.

Of the five points inclining toward a security, one is planned for remediation as CuBit™ matures its market presence. The second is debatable, depending upon the reader’s interpretation.

Of the five points inclining toward a security, one is planned for remediation as CuBit™ matures its market presence. The second is debatable, depending upon the reader’s interpretation.

- Of twelve tests listed under reasonable expectation of profits CuBit™ clearly fails eleven tests of a security and possibly fails all twelve.

- Of eight marketing tests, CuBit™ clearly does not qualify as a security for six of the tests. CuBit™ qualifies as a security by one test and may qualify as a security on a second test.

- Of six tests within reevaluation of expected profits, CuBit™ does not qualify as a security for all six.

- Of sixteen listed consumption characteristics tests, CuBit™ is clearly disqualified as a security by fifteen tests of the sixteen. Disqualification for the remaining test is possible, but unlikely, because it would require real estate to be considered a consumable product. The application of depreciation indicates consumption. Improvements (e.g., buildings, water and sewer connections, etc.) depreciate. The land itself does not depreciate.

Of the total of forty-two distinct tests in this part of Howey, CuBit™ clearly does not qualify as a security on thirty-seven tests. It might qualify as a security on three tests and appears to qualify on two tests.

More important than all these lesser tests is the foundational proposition that,

“Price appreciation resulting solely from external market forces (such as general inflationary trends or the economy) impacting the supply and demand for an underlying asset generally is not considered ‘profit’ under the Howey test.”

Because price appreciation for CuBit™ results primarily from the external forces affecting real estate values across the market, CuBit™ unequivocally does not qualify as a security under the Howey test. However, it does qualify as a currency.

Conclusions

Using CuBit™ as a replacement for fiat currencies for savings is the primary function of CuBit™. That functionality is available today. It does not depend on any future development of CuBit™.

Using CuBit™ for routine consumer purchases is a predicted development. Many features are already present. If a debit card based on CuBit™ is implemented, that utility may have an incidental effect on CuBit™ value. Because CuBit™ is a savings vehicle, based on the value of real estate, use for consumer purchases will never be a primary value driver.

Based on the overwhelming failure of CuBit™ to qualify as a security under Howey, we believe that any reasonable person will conclude that CuBit™ is not a security.

We also believe that the consumption tests demonstrate that CuBit™ is a currency.

As a commodity, such as corn, wheat, BTC, and ETH, CuBit™ is exempt from securities registration and regulation. Under the Commodities Futures Trading Commission (CFTC) rules, commodities are not inherently regulated or registered unless and until a party attempts to sell contracts, derivatives, or futures products based on that commodity. Then, it is the contract, not the commodity itself, which is regulated by the CFTC.